When you fill a prescription, you might see a charge on your card that doesn’t match what the pharmacy told you the drug costs. That’s because your health plan doesn’t pay the full price - you do, too. This shared cost is called cost sharing, and it’s made up of three parts: deductibles, copays, and coinsurance. If you’ve ever been confused about why you paid $40 one month and $120 the next for the same medication, this is why.

What Is a Deductible?

Your deductible is the amount you pay out of pocket each year before your insurance starts helping with costs. For example, if your plan has a $2,000 deductible, you’ll pay 100% of your prescription costs until you’ve spent that much. After that, your plan kicks in.

Not all medications count toward your deductible. Some plans have separate deductibles for pharmacy costs, while others combine them with medical bills like doctor visits or lab tests. High-deductible health plans (HDHPs) - common in 2026 - often require you to pay the full cost of prescriptions until you hit the deductible. That means a $500 monthly medication could cost you $6,000 a year before insurance helps.

But here’s the catch: preventive medications, like certain vaccines or blood pressure pills for high-risk patients, may be covered at $0 even before you meet your deductible. The Affordable Care Act requires this for many drugs, but it depends on your plan. Always check your Summary of Benefits to see which medications are exempt.

What Is a Copay?

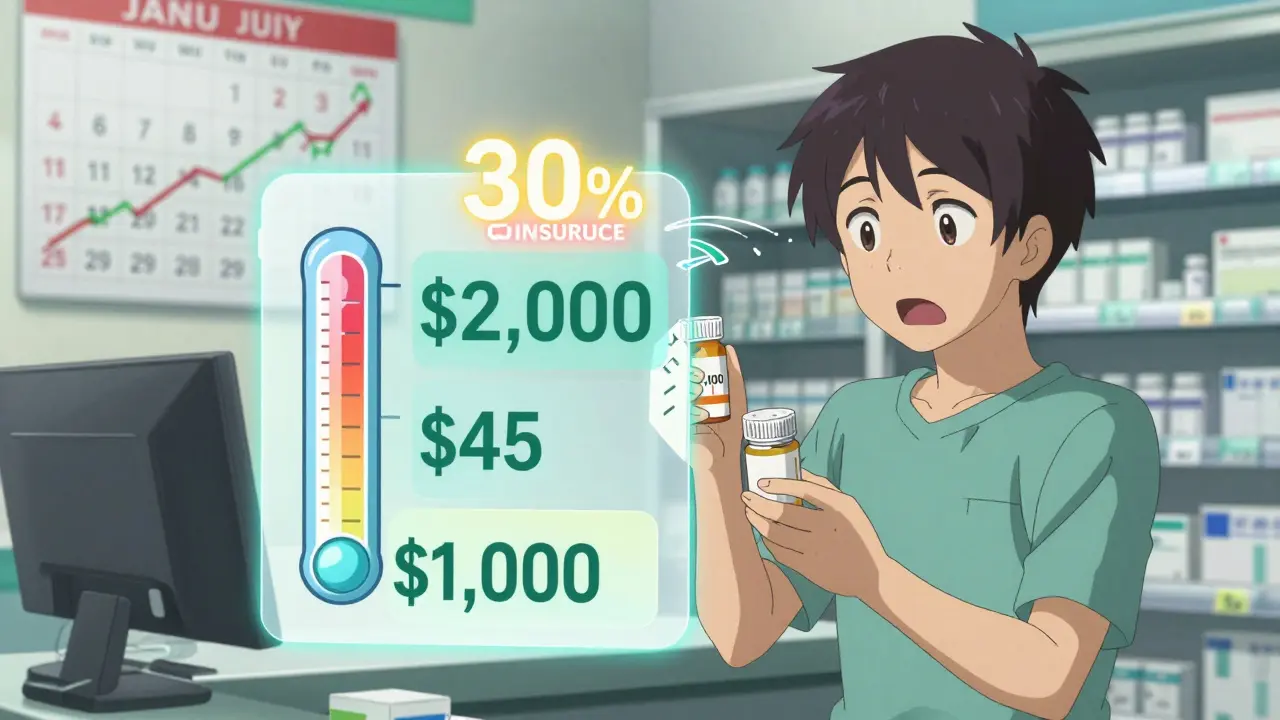

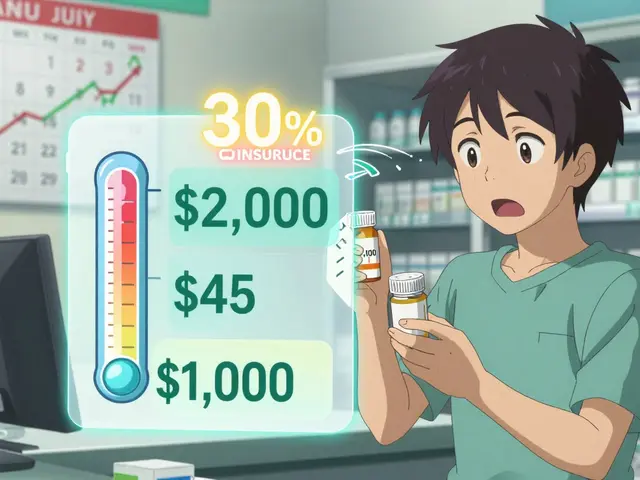

A copay is a fixed dollar amount you pay each time you get a prescription filled. It’s simple: $15 for generic, $45 for brand-name, $75 for specialty drugs. You pay this at the pharmacy counter, no matter how much the drug actually costs.

Most plans use copays for routine prescriptions. They’re predictable, which is why people prefer them. But copays don’t always apply right away. If you haven’t met your deductible, you might still pay the full price - not the copay. Some plans skip the deductible for generics, but require you to pay full price for brand-name drugs until you’ve spent your deductible amount.

For example, your plan might have a $1,500 deductible and a $20 copay for generics. The first time you fill a $120 generic, you pay $120 - not $20 - because you haven’t hit your deductible yet. Once you’ve paid $1,500 in total for covered services, your next generic fill will cost $20.

What Is Coinsurance?

Coinsurance is trickier. It’s not a fixed amount - it’s a percentage. After you meet your deductible, your plan pays a portion of the cost, and you pay the rest. Common coinsurance splits are 80/20 or 70/30.

Let’s say you have a 20% coinsurance on a $1,000 specialty drug. After your deductible is met, you pay $200. Your insurance pays $800. But if the drug’s price goes up next year to $1,200, you’ll pay $240. Coinsurance follows the price - not a set number.

This matters a lot for chronic conditions. If you’re on a $3,000 monthly medication and your coinsurance is 30%, you’re paying $900 per fill. That’s $10,800 a year. And if your plan has a $9,100 out-of-pocket maximum (the 2026 federal cap for individuals), you’ll hit that limit after about 10 fills. After that, your plan pays 100%.

Out-of-Pocket Maximum: The Safety Net

Every dollar you pay toward your deductible, copay, or coinsurance counts toward your out-of-pocket maximum. Once you hit that number - $9,100 for individuals, $18,200 for families in 2026 - your insurance pays 100% of all covered services for the rest of the year.

This is crucial for people on expensive medications. Without this cap, a single drug could bankrupt someone. But many people don’t realize premiums don’t count toward this limit. You can pay $300/month in premiums and still owe $9,100 in out-of-pocket costs before insurance covers everything.

For example, if you take three specialty drugs costing $800 each, with 30% coinsurance, you pay $240 per fill. After 38 fills, you’ll hit the $9,100 cap. That’s about 12 months. After that, your next 10 fills are free.

How Plan Types Change Your Costs

Your plan tier - bronze, silver, gold, platinum - determines how much you pay upfront versus later.

- Bronze plans: Lowest premiums, highest deductibles ($7,000+). You pay almost everything until you hit the deductible. Good if you rarely use meds.

- Silver plans: Mid-range. Deductibles around $2,500-$5,000. Often eligible for extra subsidies. Best for moderate users.

- Gold/Platinum plans: Higher premiums, low or no deductibles. You pay small copays from day one. Best for chronic conditions or expensive drugs.

If you’re on a $4,000/month medication, a platinum plan might save you $30,000 a year compared to bronze. But if you only take a $20 generic once a month, you’re wasting money on a high-premium plan.

What You Should Do Right Now

You don’t need to be a financial expert to avoid surprises. Here’s what works:

- Check your Summary of Benefits. Every insurer must give you this. Look for the section titled “Cost Sharing.” It shows real examples: how much you’d pay for a doctor visit, a hospital stay, or a prescription.

- Use your insurer’s cost estimator. Most apps let you search for your drug and see what you’ll pay at different pharmacies. Some save you 30% just by choosing a different location.

- Ask if your drug has a generic. Generics are often 80% cheaper. Your doctor can usually switch you.

- Verify in-network pharmacies. Out-of-network pharmacies might charge you 50% more - even if your plan says “coinsurance.”

- Ask about patient assistance programs. Drugmakers like Pfizer, AbbVie, and Roche offer free or discounted meds to people who qualify based on income.

One woman in Sydney, on a $2,800 monthly medication, found out her plan’s coinsurance was 40%. She paid $1,120 per fill. After calling her insurer, she learned a mail-order pharmacy offered the same drug with 20% coinsurance. She saved $5,000 a year.

Common Mistakes People Make

- Thinking copays count before the deductible - they don’t, unless your plan says so.

- Believing premiums count toward your out-of-pocket max - they don’t.

- Assuming all prescriptions count toward your deductible - some don’t, especially if they’re not on your plan’s formulary.

- Not checking if your drug is covered - 1 in 5 people get hit with a surprise bill because their medication isn’t on the list.

According to the Patient Advocate Foundation, 31% of people with chronic conditions got unexpected bills because they didn’t understand coinsurance. Most didn’t know it applied after the deductible - and that it could change with drug price hikes.

What’s Changing in 2026

The Inflation Reduction Act capped insulin at $35 per month for Medicare users - a huge win. But private plans aren’t required to do the same. Still, more insurers are starting to lower coinsurance for high-value drugs like diabetes and heart meds, while keeping it high for low-value ones.

By 2026, 60% of plans will use “value-based design,” meaning they’ll reduce your cost for drugs proven to prevent hospital visits. If you’re on a blood thinner that cuts stroke risk, your coinsurance might drop to 10%. If you’re on a supplement with no proven benefit, it might jump to 50%.

Also, new rules require insurers to show you your estimated out-of-pocket cost before you fill a prescription - just like a price tag at a store. No more surprises.

Do copays count toward my deductible?

Usually not. Most plans require you to pay your full deductible before copays kick in. But some plans, especially for generics, let you pay a copay even before meeting the deductible. Always check your plan’s rules - it varies.

What if I can’t afford my coinsurance?

Many drug manufacturers offer patient assistance programs. You can also ask your pharmacy about discount cards like GoodRx or RxSaver. Some states have prescription assistance funds for low-income residents. And if you hit your out-of-pocket maximum, your plan pays 100% for the rest of the year - so keep track of what you’ve spent.

Can my deductible be different for pharmacy vs. medical costs?

Yes. Some plans have separate deductibles: one for doctor visits and hospital stays, another for prescriptions. Others combine them. Your Summary of Benefits will say which one applies. If it’s not clear, call your insurer and ask: "Do pharmacy and medical costs count toward the same deductible?"

Why did I pay more for the same drug last month?

Two reasons: either the drug’s price went up, or you’re in coinsurance and your plan’s allowed amount changed. Coinsurance is a percentage of the cost - so if the drug costs more, you pay more. Also, some pharmacies charge different prices. Try switching to a mail-order or in-network pharmacy.

Does Medicare have different cost-sharing rules?

Yes. Medicare Part D (prescription drug coverage) has its own deductible, coverage gap (donut hole), and catastrophic coverage. In 2026, the deductible can be up to $590. After that, you pay 25% coinsurance until you hit $8,000 in out-of-pocket costs. Then, catastrophic coverage kicks in - you pay 5% or a small copay. The Inflation Reduction Act also capped insulin at $35/month and eliminated the donut hole for brand-name drugs.

If you’re on long-term medication, understanding cost sharing isn’t just helpful - it’s essential. A few minutes reviewing your plan could save you thousands. Don’t wait for the bill to arrive. Ask questions. Use the tools. Know your numbers.

Oh wow, this is so clear now. I thought my $120 charge was a mistake last month, but now I get it - coinsurance is just a percentage of whatever price they decide to charge that day. No wonder I keep getting billed differently. My pharmacy doesn’t even tell me the actual cost, just says 'your insurance paid part.' Yeah, right. 🙄

Cost sharing mechanics are fundamentally aligned with risk pooling principles. Deductibles function as a threshold filter to reduce moral hazard. Copays enforce behavioral discipline. Coinsurance ensures proportional responsibility. The system isn’t broken - it’s optimized for sustainability. Most users lack the systems literacy to parse this.

i just paid $800 for my blood pressure med and i swear i thought i was getting ripped off. turns out i was in the donut hole? wait no, i dont even have medicare. why is this so confusing?? my phone bill is easier to understand. someone help. 🤯

Everyone’s acting like cost-sharing is some new invention. Nah. It’s been around since the 80s. The real issue? Insurance companies raised drug prices 400% in 5 years and now they want YOU to pay more for it. The system’s rigged. Stop blaming patients.

Just got my new insulin prescription 😍 $35!!! I cried. I didn’t think this day would come. If you’re on meds, DO NOT skip checking if your drug’s on the new list. I saved $400/month. Thank you, IRA. 🙏❤️

One thing nobody talks about: formulary tiers. Your plan might say 'generic copay $15' - but if your drug isn’t on Tier 1, you’re paying brand-name prices. Always check the tier, not just the copay number. I learned this the hard way when I got stuck with a $220 charge for a 'generic' that was actually Tier 3. Called my insurer. Got it switched. Took 12 minutes. Do this.

It’s wild how something as simple as a percentage can break people. Coinsurance isn’t math - it’s emotional labor. You’re not just paying money, you’re paying anxiety. Every time your drug price ticks up, you feel like you’re failing. I’ve been on 3 different meds in 2 years. Each time, I had to relearn the whole system. It’s exhausting. We need better UX in healthcare. Not more jargon.

Let’s be real: the entire system is a Ponzi scheme disguised as 'affordable care.' Deductibles? Just a way to delay payouts. Coinsurance? A trick to make you think you’re 'sharing' - when really, they’re just shifting risk onto you. And don’t get me started on 'out-of-pocket maximums' - those are just marketing tools. They’ll change the rules next year. You think you’re safe? You’re not.

They’re lying about the 2026 changes. The Inflation Reduction Act doesn’t apply to private insurers - that’s a myth. Big Pharma and Blue Cross are quietly raising prices to offset the $35 insulin cap. I’ve seen the internal memos. You think you’re protected? You’re being manipulated. Check your EOBs. Look for 'allowed amount' adjustments. It’s all smoke and mirrors.

Use GoodRx. Always. I paid $12 for a $300 drug last week. Just typed the name. Found a local pharmacy. Paid cash. No insurance needed. It’s not magic. It’s just not being lazy.

Oh honey, you paid $6,000 for a pill? And you thought it was 'fair'? Sweetie. You didn’t get scammed. You got schooled. Next time, read the tiny print before you sign up. Or better yet - don’t buy the cheapest plan. You’re not saving money. You’re just gambling with your health. And that’s not brave. It’s dumb.

Stop whining. You want affordable meds? Work for a company that offers platinum plans. Or move to Canada. Or ask for generics. Or use mail order. Or apply for assistance. There are options. You’re not helpless. You’re just used to being coddled.

Y’all are making this way too complicated. It’s simple: insurance is a scam. They charge you monthly, then act surprised when you need help. I had a $1,000 med. They said I owed $300. I called. They said 'oh wait, your deductible was met last week.' So why didn’t they tell me that before I paid? Because they want you to feel stupid. And you did. Good job.

As someone from the Philippines who moved to the U.S., I’m shocked how much more complicated this is than in my home country. Here, you need a PhD just to fill a prescription. In Manila, I paid $5 and left. No forms. No tiers. No coinsurance. Just medicine. Maybe we’re over-engineering healthcare.

I used to hate my gold plan. $500/month premiums. Felt like a rip-off. Then I got hit with a $4,500 drug bill - and paid $0. Because I hit my out-of-pocket max 3 weeks in. That plan saved my life. Stop judging high-premium plans. Sometimes they’re the quiet heroes.