Every year, millions of Americans face surprise medical bills, hidden fees, and aggressive debt collection tactics - even when they thought they were covered. In 2025, patient rights are stronger than ever, especially in New York, where new laws have rewritten how healthcare providers handle consent, payments, and financial products. These aren’t just paperwork changes. They’re real shields against predatory billing practices that have left families drowning in medical debt.

What’s Changed in New York’s Patient Protection Laws?

As of October 20, 2024, New York enacted three major laws designed to protect patients from financial exploitation in healthcare. These laws target three key areas: how providers get your consent, how they handle payment applications, and when they can ask for your credit card.

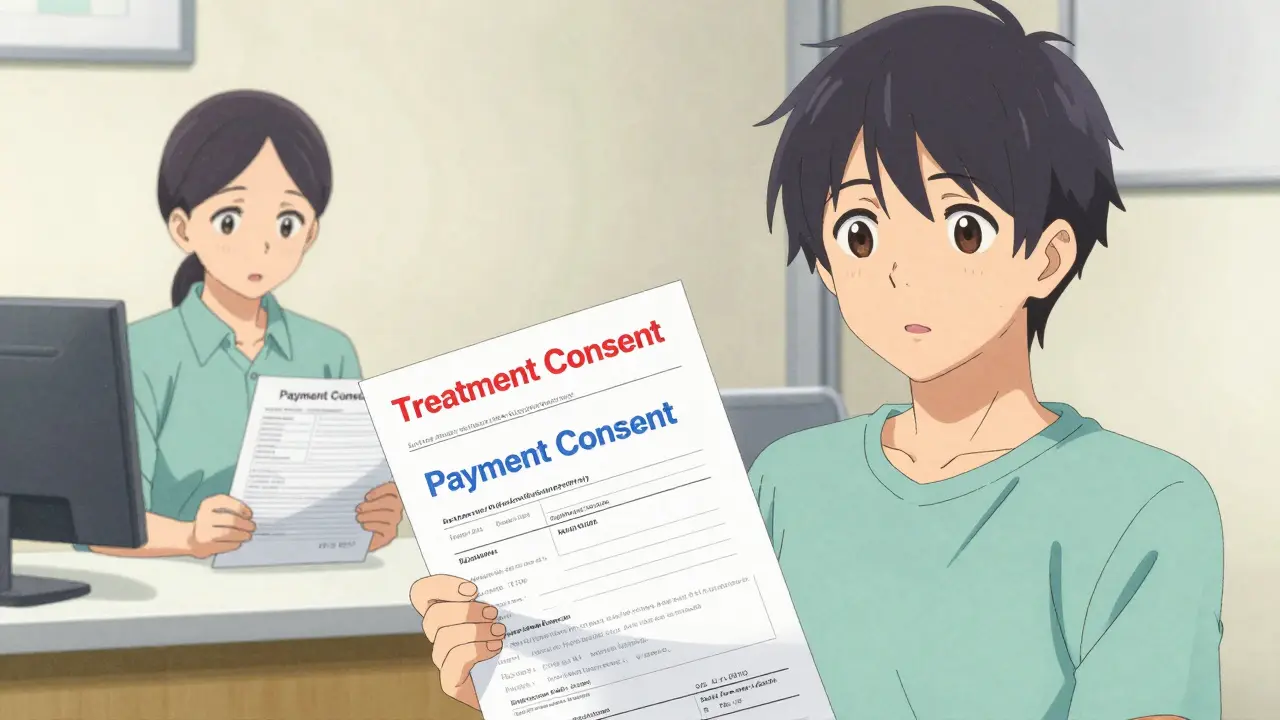

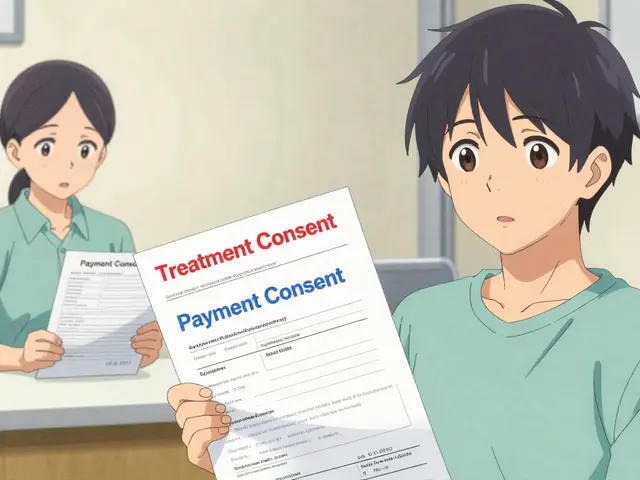

Before these rules, it was common for clinics to hand you a stack of forms on your first visit. One form would ask you to sign for both treatment and payment authorization - often in tiny print. Now, under Public Health Law Section 18-c, providers must get your separate, clear consent for treatment and for payment. You can’t sign one form that covers both. Violating this rule costs providers $2,000 per incident.

But here’s the twist: as of August 7, 2025, enforcement of Section 18-c has been suspended. That doesn’t mean the law is gone - it means clinics are waiting for clearer guidance from the state. Until then, many providers are still separating consent forms as a precaution. You should too. Always ask: Is this for treatment? Or for payment?

Don’t Let Providers Fill Out Your Medical Financing Apps

Have you ever been handed a CareCredit® application at the doctor’s office? Maybe the front desk staff said, “I’ll just help you fill this out real quick.” That’s now illegal under General Business Law Section 349-g.

Providers can answer your questions. They can explain terms. But they cannot touch the application. Not one field. Not even your name. The form must be completed entirely by you. Why? Because if the provider helps, they’re seen as pushing you into a financing plan - and that’s a conflict of interest. Fines for breaking this rule? Up to $5,000 per violation.

This law shuts down a common trick: clinics pushing patients into high-interest medical credit cards because they get kickbacks from lenders. Now, you’re the one in control. If someone tries to help you fill it out, say no. Take the form home. Read it. Compare options.

Why Your Credit Card Could Be Riskier Than You Think

Under General Business Law Section 519-a, providers can no longer require you to give them your credit card on file before emergency or necessary care. No more “we need your card to process this” before you get an MRI or stitches.

Even more important: if you do pay with a regular credit card - like Visa or Mastercard - you lose access to legal protections that apply to healthcare-specific financing. That means:

- Your medical debt can still show up on your credit report

- Doctors can garnish your wages

- They can place liens on your home

But if you use a healthcare financing product like CareCredit® - and you follow the rules - you’re protected by federal and state rules that block wage garnishment, credit reporting, and liens on your primary residence. The catch? You have to use the right tool.

Providers must now tell you this in writing every time you use a traditional credit card. That notice? It’s not optional. It’s required by law. If you didn’t get it, ask for it. Keep a copy.

How These Laws Compare to Federal Protections

The federal No Surprises Act (effective January 1, 2022) protects you from surprise bills when you see an out-of-network provider by accident - like an anesthesiologist you didn’t choose. But it doesn’t touch the everyday financial traps: consent forms, credit card grabs, or hidden financing pressure.

New York’s laws go further. They protect you even when you’re seeing an in-network doctor. They stop providers from using your medical visit as a sales pitch for debt. They force transparency where federal law stayed silent.

And then there’s the Consumer Financial Protection Bureau (CFPB) rule from 2024 - which removed medical debt from credit reports entirely. That’s huge. But it only applies to debts incurred through healthcare financing products, not regular credit cards. So if you paid your $8,000 surgery bill with your Chase card, you’re still at risk. If you used CareCredit®, you’re protected.

This is why the distinction matters. It’s not just about the bill amount. It’s about how you pay it.

What You Should Do Right Now

These laws are useless if you don’t know how to use them. Here’s your action plan:

- Separate your consents. If you’re asked to sign one form for treatment and payment, ask for two separate forms. Say: “I need to review my consent for care and my consent for payment separately.”

- Never let anyone fill out your financing application. Take the CareCredit® or similar form home. Read the interest rate, term, and penalty clauses. If you’re unsure, call the lender directly.

- Ask for the credit card risk notice. Every time you pay with a regular credit card, the provider must give you a written warning about losing medical debt protections. If they don’t, ask for it. If they refuse, file a complaint with the New York State Department of Health.

- Use healthcare financing wisely. If you need to finance care, use a product designed for medical expenses - not your personal credit card. Compare APRs, grace periods, and repayment terms. Many offer 0% for 12-24 months.

- Keep records. Save every consent form, payment notice, and financing agreement. If a bill shows up you didn’t agree to, you’ll need proof.

What This Means for Your Rights in 2025

Medical debt affects 100 million Americans, totaling $195 billion. New York’s laws are the most aggressive state-level response to this crisis. They don’t just tweak forms - they shift power back to patients.

These rules aren’t perfect. The suspension of Section 18-c creates confusion. Not all providers are trained. Some still push credit cards because they’re easier than explaining financing options.

But the trend is clear: regulators are no longer ignoring the financial harm of healthcare. Other states are watching New York. California, Illinois, and Massachusetts are already drafting similar bills. The days of clinics treating your wallet like an afterthought are ending.

Your body is yours. Your money should be too.

Do these New York laws apply to me if I live outside the state?

These laws only apply if you receive care from a provider based in New York. But if you’re treated in New York - even if you’re from another state - you’re protected under these rules. If you live elsewhere but get care in New York, you can still use these protections. The location of the provider, not your residency, determines which laws apply.

What if my doctor says they don’t use CareCredit® or similar financing?

That’s fine. You still have rights. Even if your provider doesn’t offer medical financing, they must still give you separate consent forms for treatment and payment. They also must warn you in writing if you pay with a regular credit card - explaining that you’ll lose medical debt protections. If they don’t, file a complaint with the New York State Department of Health.

Can a provider refuse to treat me if I don’t sign a payment consent form?

No. Under federal and state emergency care laws, providers cannot deny treatment for emergencies or medically necessary services based on payment consent. However, they can refuse to schedule non-emergency procedures until you provide consent. If you’re being pressured or denied care for an urgent issue, call the New York State Department of Health hotline immediately.

Are there penalties for patients who misuse these laws?

No. These laws are designed to protect patients, not punish them. There are no fines or legal consequences for patients who ask for separate consents, refuse to let staff fill out applications, or choose not to use credit cards. You’re exercising your legal rights - not breaking any rules.

How do I report a provider who violates these laws?

File a complaint with the New York State Department of Health’s Patient Protection Division. You can do it online at health.ny.gov or by calling 1-800-810-6582. Keep copies of all forms, receipts, and communications. The department investigates all complaints and can issue fines to providers. You can also report violations to the Consumer Financial Protection Bureau at consumerfinance.gov/complaint.

Just had my first MRI last week and they tried to hand me one form for everything. I said nope, separate them. They looked confused but gave me two. Felt like I just won a tiny battle against the machine. Keep doing this, folks.

It’s wild how something as simple as asking for two forms can feel like a radical act. But it’s not. It’s just basic human dignity. We’ve been conditioned to sign anything shoved at us. Time to unlearn that.

Oh please. These laws are just performative activism. Providers are still gonna push CareCredit® because people are dumb and scared. You think a piece of paper stops someone from signing under pressure? LOL.

lol why u so serious? 😅 i used my credit card for my mom’s surgery and she’s fine. why u wanna make everything so complicated? 🤷♂️

man i didnt even know this was a thing. i just signed whatever they put in front of me. now im gonna start asking for separate forms. no more rushing. i got my health and my wallet to protect. thanks for this

Another law that’s unenforceable and ignored. Wake up. Providers don’t care. You think they’ll risk $2k when they can just lie and say you signed it?

Let me just say this - I sat in a waiting room for 90 minutes after my knee surgery because the billing department was ‘waiting for approval’ from the financing company they ‘helped’ me sign up for. I didn’t even know I’d agreed to 24% APR. That’s not a mistake. That’s a trap. And now? Now I’ve got the law on my side. I’m not just relieved - I’m furious. And I’m telling everyone I know.

soooo… if i use my chase card, i lose all protections? cool. so i’ll just use carecredit® then. 🤷♂️ btw that 0% for 18 months is still a trap if you miss one payment. just saying.

I just want to say thank you to the person who wrote this. I’ve been scared to speak up for years. I thought I was being ‘difficult.’ Turns out, I was just right. I’m printing this out and keeping it in my wallet. Every time I go to the doctor now, I pull it out. It’s my little armor.

They’ll still push credit cards. But now? Now you’ve got the law in your back pocket. And that’s enough to make them sweat. I’ve seen it - when patients say ‘I know my rights,’ the whole vibe changes. The smile gets tighter. The pen slows down. That’s victory.

These laws are beautiful. Not because they’re perfect, but because they say: you matter. Even when you’re in pain. Even when you’re scared. Even when you’re tired. You still get to say no. And that’s more powerful than any form.